Onchain Execution: Gas, Venue Selection, and Netting in Multi-Vault Rebalancing

How Orion's framework supports capital-efficient strategies with intent-based execution, venue selection, and order netting.

For a manager deploying strategies on Orion, the relevant question is whether the infrastructure supports onchain portfolio management with competitive execution economics.

Two Components of Execution Cost

Gas is the cost of expressing a rebalance onchain, telling the protocol what the target portfolio should be. Liquidity cost is the cost of achieving it, moving assets through liquid venues to achieve the target exposure. Orion separates these cleanly: managers submit intents; the protocol handles settlement and routing through a curated investment universe.

Beside simplifying onchain execution, the separation is an economic design choice. Managers incur gas only at intent submission; settlement and routing are handled downstream by the protocol.

Gas Costs

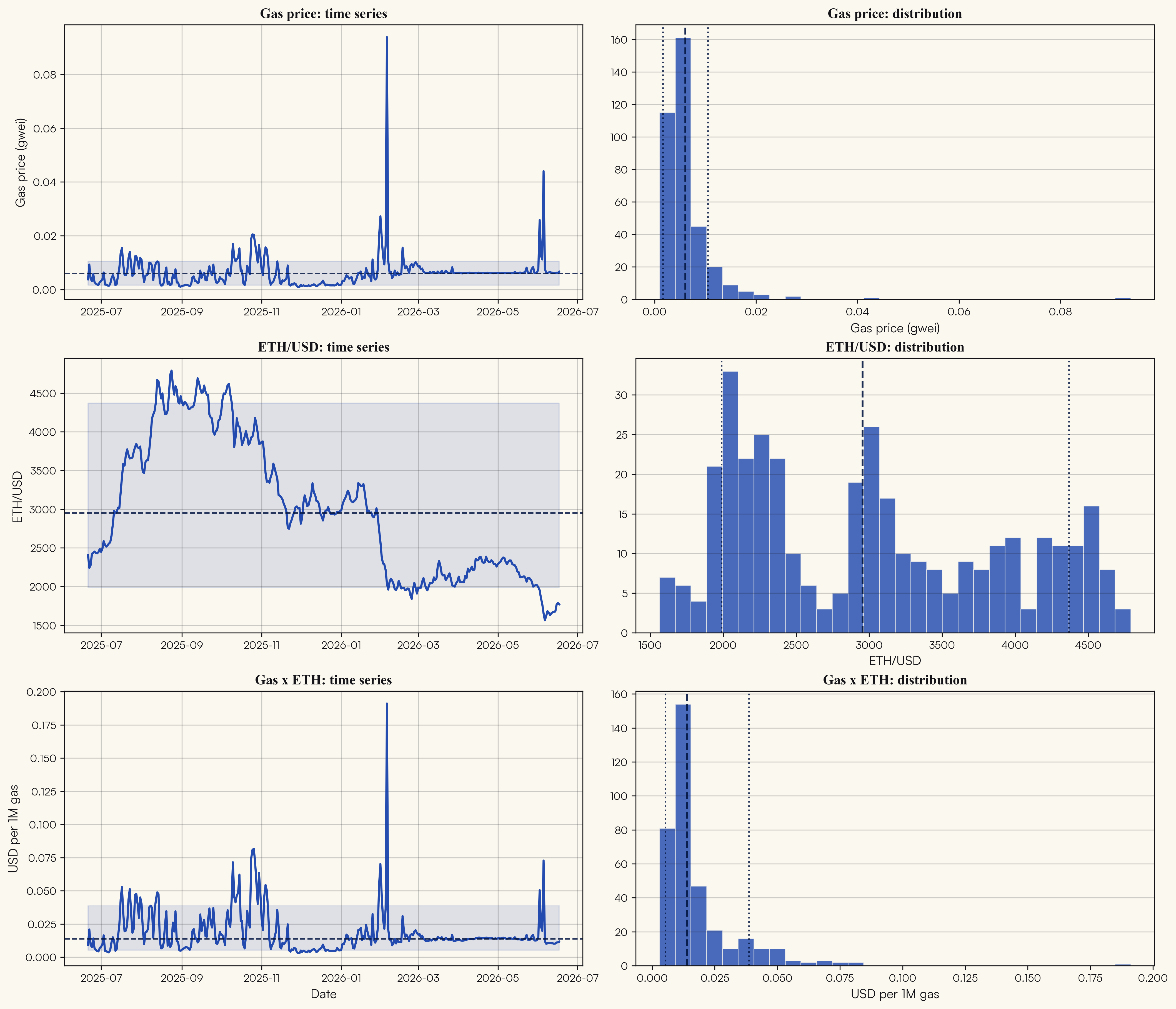

Portfolio managers need a view of gas costs. That cost is not well represented by gas price alone. Dollar expense is the product of network congestion (gas price in gwei) and the ETH/USD rate at execution.

The chart below plots daily gas price, ETH/USD, and the resulting USD cost per million gas units.

The baseline regime is favorable: gas spends most of the sample at low levels, and even when ETH is elevated, the joint cost per gas unit remains manageable. As ethereum.org's 2026 builder overview notes, mainnet is no longer priced like a permanently congested chain, a structural change that matters for portfolio programs batching state transitions on L1 rather than routing operational logic to rollups by default.

Intent Submission as the Manager's Gas Boundary

On Orion, the manager-facing gas obligation is confined to intent submission: the Layer-1 call that expresses target weights across vaults. Settlement, routing, and swap execution occur downstream and do not appear as separate gas line items on the manager's side.

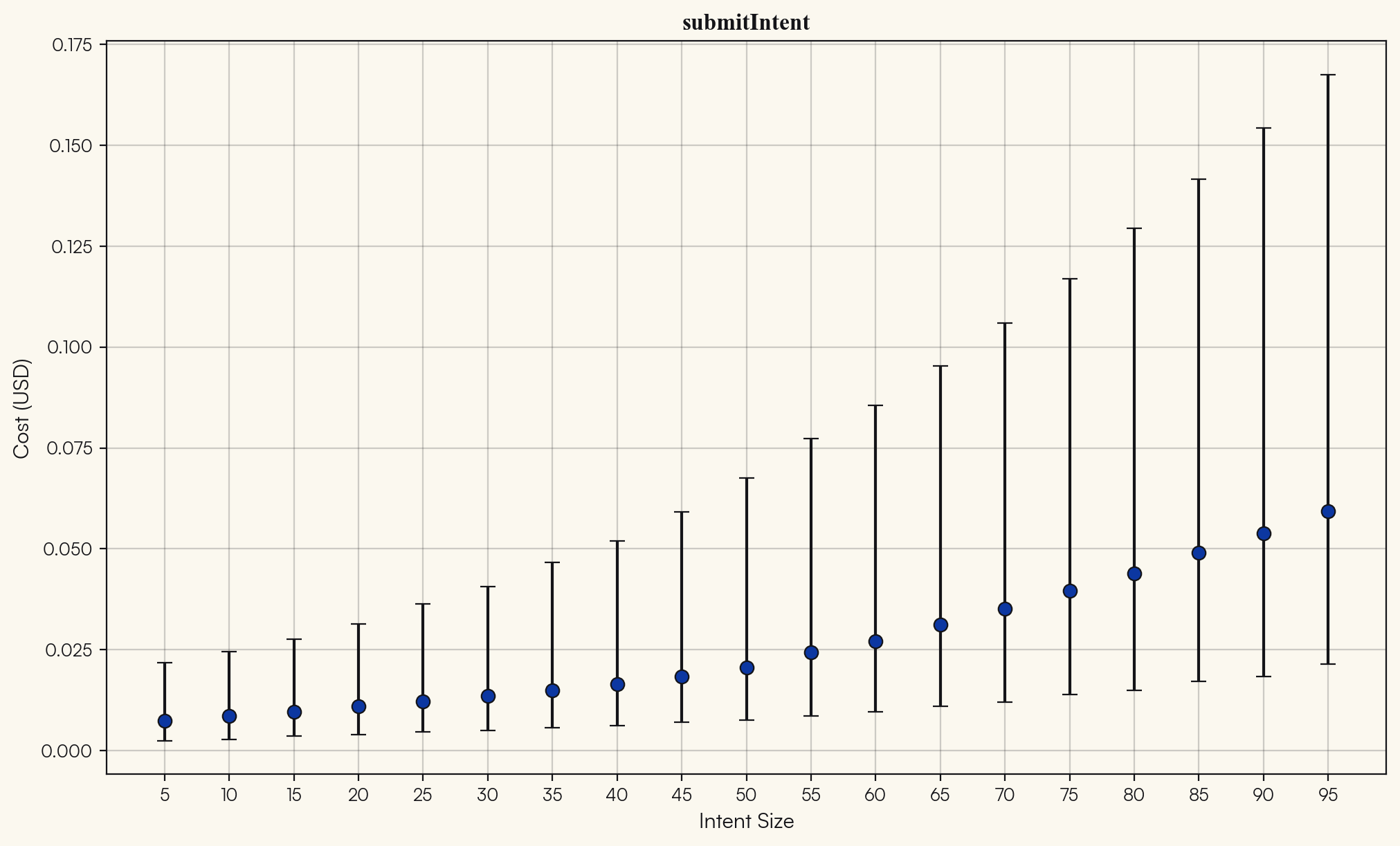

The chart below maps submission cost in USD against intent size, a proxy for rebalance complexity, with confidence intervals reflecting the impact of other variables.

Even at large intent sizes, submission cost remains in cents, not dollars. Cost rises with complexity, and the upper uncertainty band widens at scale, but the absolute level is negligible relative to vault NAV. For systematic rebalancing programs, Layer-1 gas does not bind rebalancing decisions.

The practical implication is that execution economics are dominated by liquidity, not by Layer-1 overhead.

Execution Across the Investment Universe

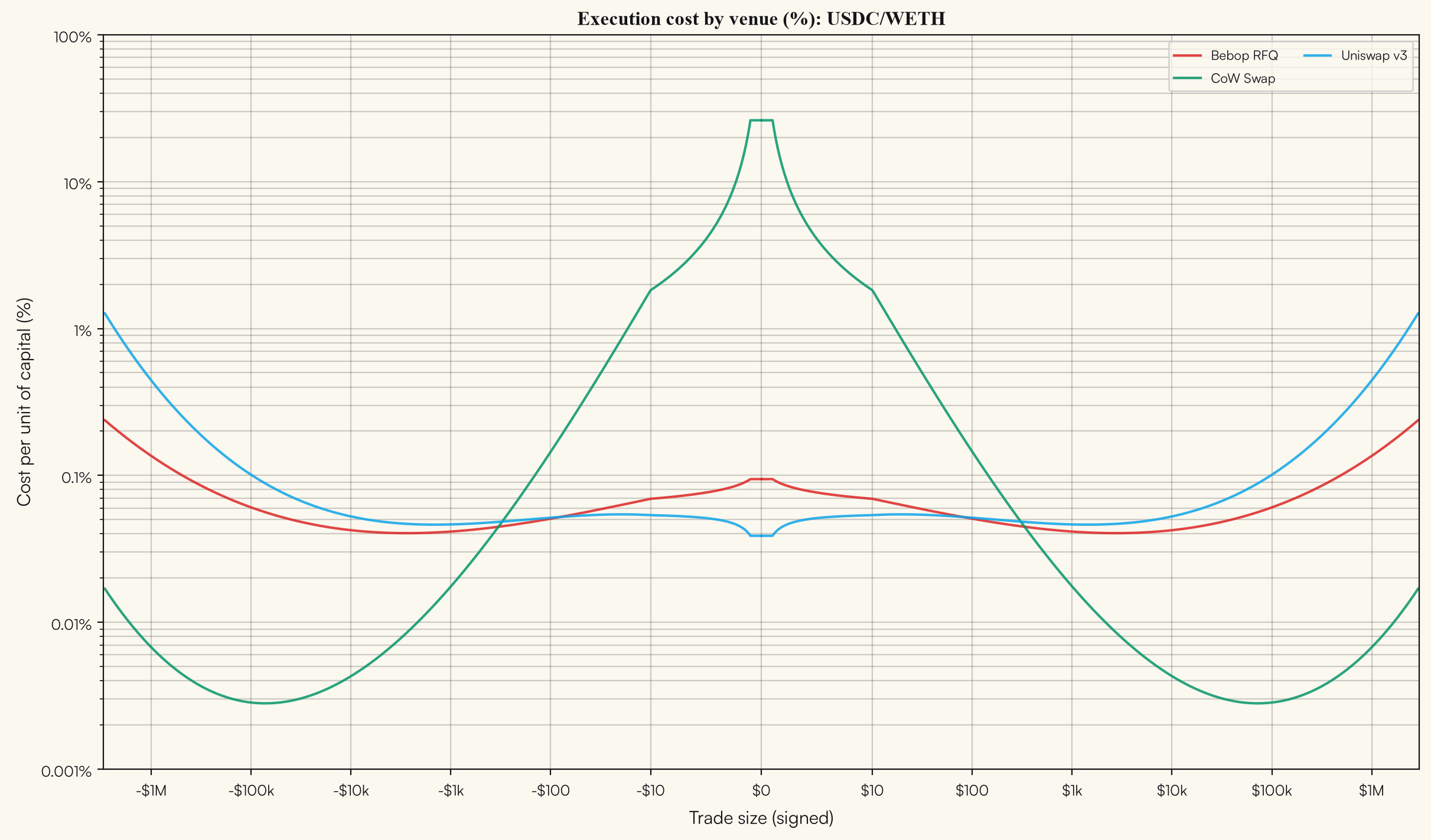

Residual portfolio flow is routed through three venue types. Costs below use η = 0 (no internal netting).

| Venue | Role |

|---|---|

| Uniswap v3 | Continuous AMM from pool state |

| Bebop | Professional MM RFQ |

| CoW Swap | Batch auction |

Cost per unit of capital (%):

Uniswap v3 shows the classic fee-floor plateau, then convex slippage at size. Bebop RFQ is relatively flat in percentage terms, with less size dependence than the AMM tail. CoW Swap is U-shaped: elevated % cost at very small notionals where fixed overhead dominates, then compression at mid-to-large sizes where batching and solver competition improve terms. CoW is not cheapest at every size, but it undercuts the other venues in the rebalance-relevant band. Venue selection is a first-order decision for systematic exposure adjustments.

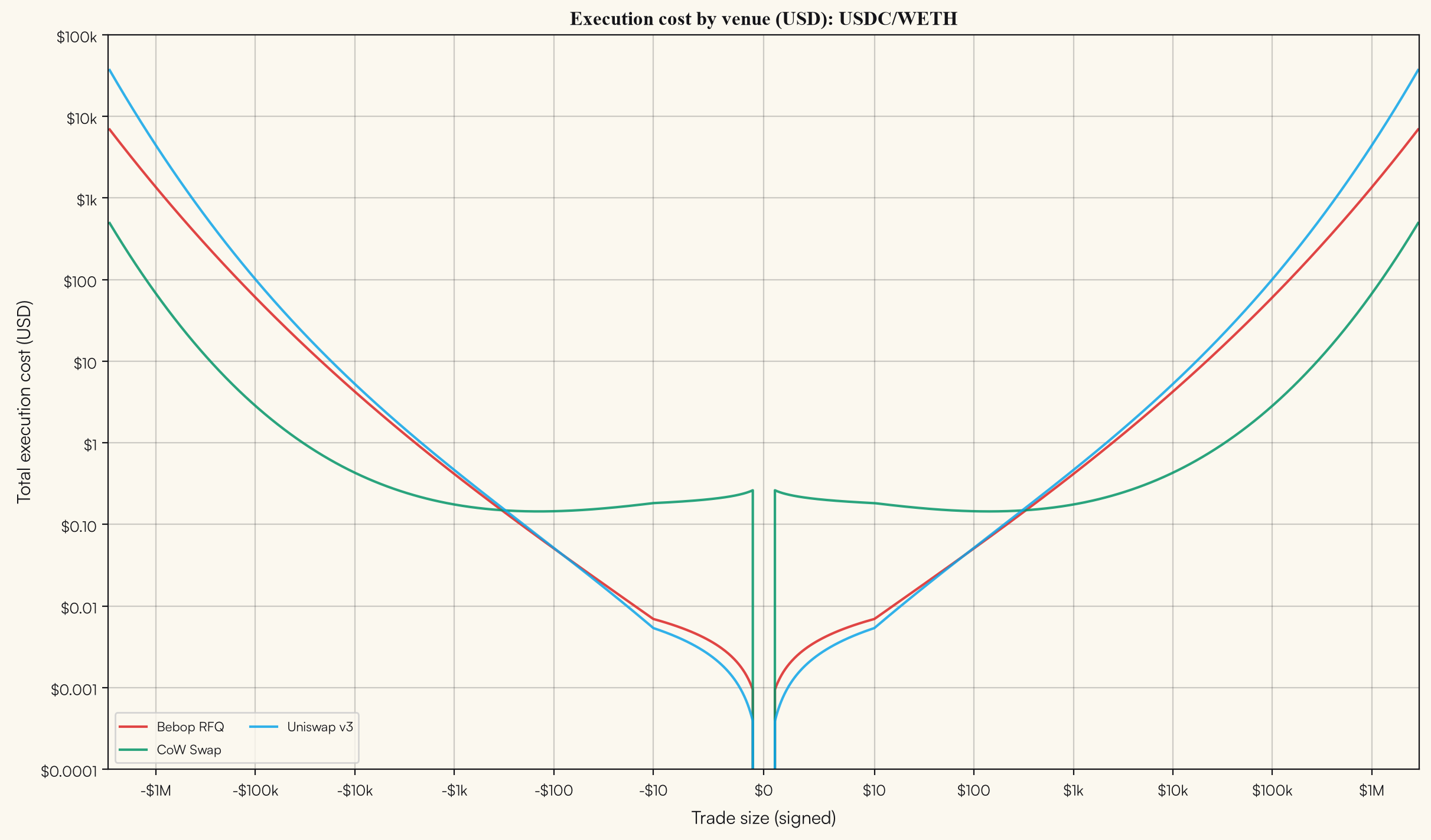

Total execution cost (USD):

In absolute dollars, CoW offers the lowest execution bill at rebalance-relevant magnitudes; Bebop is a strong RFQ alternative; Uniswap is the passive-liquidity reference.

Internal Netting and Capital Efficiency

A manager operating a single vault in isolation bears the full liquidity cost of every external rebalance leg. Orion's multi-vault architecture permits internal netting: when one vault increases exposure to an asset and another decreases it, offsetting flow is cancelled before reaching external markets.

This is the onchain analogue of dealer-market internalization: intermediaries first seek to offset heterogeneous order flows within their own books and only externalize residual inventory to the broader market. Francis-Staite (2022) formalizes the multi-portfolio analogue, internal rebalancing processes that allocate assets between books before external trading, while Barzykin et al. (2021) models the dealer case. On shared Orion infrastructure, portfolio managers rebalance against one another before reaching AMM liquidity, reducing transaction costs and preserving capital.

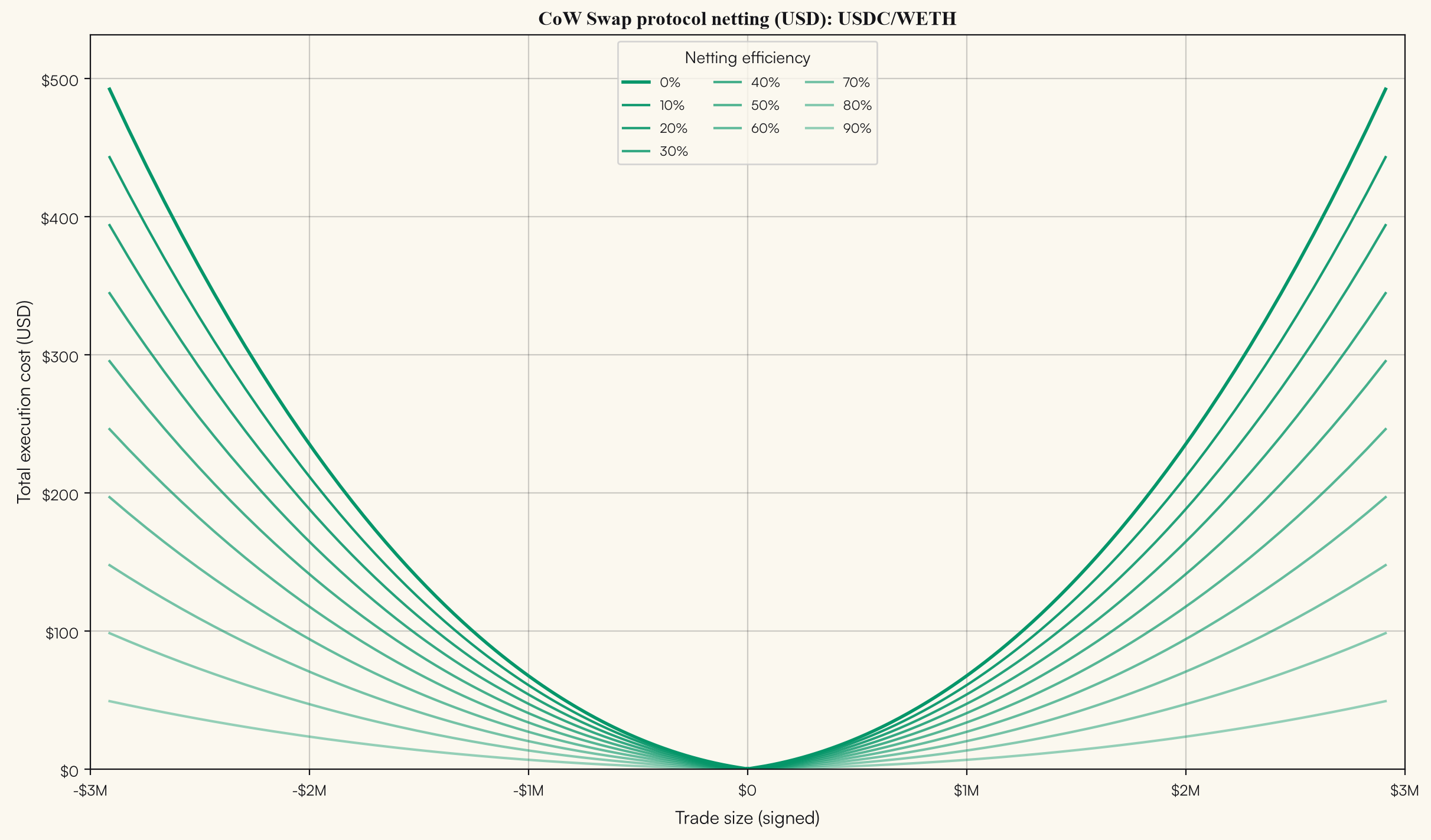

The chart below shows aggregate system execution cost at varying netting efficiencies: the fraction of gross flow offset internally before reaching external venues.

The vertical displacement between curves quantifies the capital-efficiency gain from shared infrastructure. At zero netting efficiency, the system pays full liquidity cost on gross flow. As internal offset increases, effective trade size against pool depth falls, and aggregate cost compresses toward a fraction of the isolated-vault level.

For portfolio managers, three implications follow:

- Aggregate rebalance volume can grow without proportional execution drag, provided vaults under common management generate offsetting flow.

- Netting keeps effective trade size in the fee-floor region even when gross program size would otherwise enter the slippage tail.

- Multi-vault infrastructure converts correlated rebalancing needs into execution savings: the platform is structurally more capital-efficient than the sum of independently operated vaults.

Implications for Portfolio Managers

| Cost layer | Operational character | Implication |

|---|---|---|

| Intent submission gas | Cents per rebalance | Immaterial relative to NAV |

| Venue routing (USDC/WETH) | Venue- and size-dependent | CoW preferred at rebalance-relevant scale |

| CoW netting | Linear compression in η | Material USD savings at moderate-to-high offset |

| Uniswap baseline | Fee floor + slippage | Passive reference only |

Relative to independently wired vaults, the same onchain liquidity supports lower effective execution cost and a cleaner separation between expression (intent) and achievement (liquidity).

Conclusion

Onchain portfolio management carries two execution costs with distinct drivers and scaling properties.

For Orion managers, gas is confined to intent submission and remains immaterial across intent sizes and market conditions. Liquidity cost is pool and size-dependent, and competitive for deep onchain venues. Netting across vaults further compresses aggregate cost, improving the economics of multi-strategy deployment relative to isolated rebalancing.

References

- Francis-Staite, K. (2022). Multi-portfolio internal rebalancing processes: Linking resource allocation models and biproportional matrix techniques to portfolio management. arXiv:2201.06183.

- Barzykin, A., Bergault, P., & Guéant, O. (2021). Algorithmic market making in dealer markets with hedging and market impact. arXiv:2106.06974.

- Uniswap Labs. Uniswap v3 Core.

Frequently Asked Questions

- What gas obligations does a manager incur on Orion?

- Intent submission only. Settlement and swap execution are handled downstream by the protocol.

- Why not route everything through Uniswap?

- Uniswap provides continuous passive liquidity but convex slippage at size. RFQ (Bebop) and batch-auction (CoW) routes are often more competitive for systematic flow in the rebalance-relevant notional range.

- What does netting efficiency mean operationally?

- η is the fraction of gross rebalance flow offset across vaults before residual flow reaches external venues. Effective quoted cost scales by (1 − η).

- How does multi-vault netting affect execution cost?

- When vaults under common management generate offsetting flow, internal netting reduces effective notional against external venue depth. Aggregate liquidity cost falls accordingly: managers can run larger gross rebalance programs at lower per-dollar execution cost than isolated vaults would.

- Why deploy multiple strategies on shared Orion infrastructure?

- Shared infrastructure converts correlated rebalancing needs into netting savings. Layer-1 gas economics are similar either way; the execution advantage accrues with strategy count and the degree of offsetting flow across vaults.